Generative AI in Insurance Industry

Use Cases, Roadmap & FREE Tools

Insurance still runs on PDFs, endless phone calls, and waiting weeks for what should take hours.

And while you wait, money leaks.

Nearly $34 billion is lost annually to claims leakage, plus frustrated customers often jump ship after just one slow claim experience.

Generative AI in insurance is your tireless, always-on teammate that can read 10,000 pages of regulation, draft coverage letters, and personalize quotes, before your coffee cools down.

Below, we’ll break down how it works in insurance, its applications and challenges, and provide a 1-year roadmap with free resources that you can hand to your team today to start making AI work—not just talk.

Key Highlights

Definition:

Generative AI in insurance uses advanced language and vision models to analyze data, draft documents, automate claims, and personalize coverage.

Market Momentum:

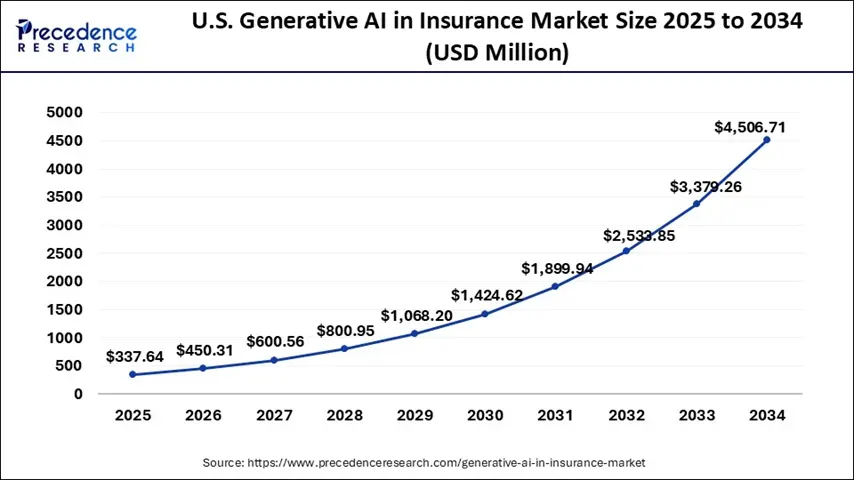

The global generative AI in insurance market is projected to grow from $1.09B (2025) → $14.30B (2034) at 33% CAGR.

Key Applications:

Key generative AI use cases in the insurance industry include claims processing, underwriting, fraud detection, policy generation, and customer support.

Common Limitations:

- Legacy system integration

- Poor data quality

- Compliance complexity

- Workforce fears

- Uncertain ROI

Deployment Strategy:

Follow a three-phase roadmap:

- Phase 1: Assess data, readiness, and pick low-risk use cases.

- Phase 2: Pilot with measurable KPIs and avoid “pilot purgatory.”

- Phase 3: Scale what works, train teams, and continuously optimize.

Free Resources in this Guide:

The Business Case: Why Insurance Companies Are Racing to Adopt GenAI

Insurance companies are not just kicking the tires on generative AI (GenAI)—they are flooring it. The global market is set to explode from $1.09 billion in 2025 to $14.30 billion by 2034, growing at a 33% CAGR.

This boom is a full-scale reinvention of how insurers operate, compete, and win.

The question is not whether your company will adopt gen AI, but whether you will be leading the pack or scrambling to catch up.

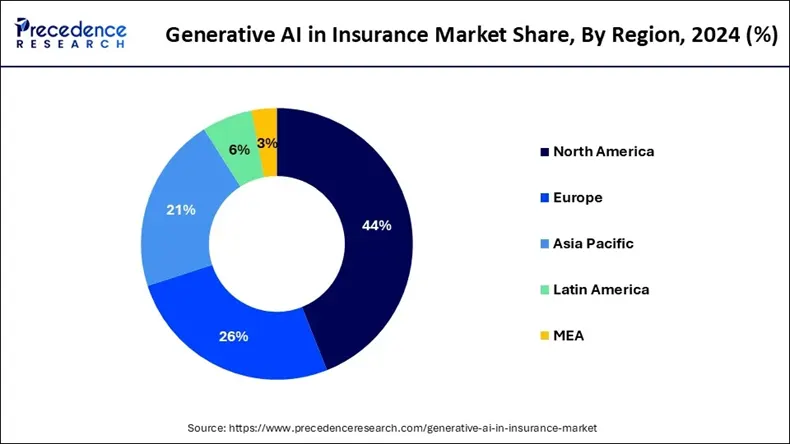

Market Growth and Investment Trends

The numbers tell a clear story. North America dominates with 44% market share, followed by Europe at 28% and Asia Pacific at 25%.

Here's a detailed regional breakdown:

Investment in generative AI in the insurance market is skyrocketing. And, you do not need a billion-dollar budget to start seeing returns.

Smart deployment of gen AI in targeted areas like claims automation or fraud detection can deliver measurable ROI within quarters, not years.

Proven ROI and Performance Metrics

Now, let us talk about the results that actually come from using generative AI in the insurance industry (based on CoinLaw & IBM data) :

- 90% of finance companies report 6%+ revenue gains from AI adoption

- Half of them doubled employee productivity

- Claims processing time came down 73%

- Customer retention is up 14%

- Net Promoter Scores are up 48%

- Premium accuracy improved by 53%

These are not projections—they are metrics from insurers already in the game.

Key Applications of Generative AI in the Insurance Market

Generative AI accelerates decisions, detects fraud patterns humans miss, and personalizes experiences at scale.

Here's where GenAI delivers the biggest impact in insurance right now:

Underwriting Operations and Risk Assessment

Underwriting has always been data-heavy and time-consuming. GenAI changes that equation entirely.

Key Applications:

- Risk assessment from unstructured data (broker submissions, financial statements, inspection reports)

- Policy document generation customized at scale

- Natural language queries for risk appetite and guideline searches

- Synthetic data generation for model training without compromising privacy

The technology analyzes complex commercial P&C submissions in hours instead of days.

Underwriters can now ask questions like "What's our risk appetite for coastal properties?" and get instant answers based on company guidelines.

— Insurance Domain Expert, Aegis Softtech

Claims Management & Fraud Detection

Claims processing is where GenAI truly flexes its muscle. The technology automates review workflows and catches fraud that traditional systems miss entirely.

Key Applications:

- Automated claims review and triage

- Image and document analysis for damage assessment

- Fraud detection through pattern recognition and anomaly identification

- Claims communication generation (denial letters, status updates, payment authorizations)

The technology trains on synthetic fraud scenarios, learning to spot linguistic patterns and documentation inconsistencies that rule-based systems miss.

— Lead AI Research Scientist, Aegis Softtech

Customer Experience and Support

Insurance has never been known for stellar customer experience. GenAI is changing that narrative, though not without challenges.

Key Applications:

- 24/7 multilingual chatbots using NLP for policy queries and self-service

- Conversational AI insurance agents run coverage eligibility checks with plain-English explanations

- Personalized policy recommendations based on individual circumstances

- Interactive knowledge bases that empower agents with instant answers

- Sentiment analysis from customer interactions for continuous improvement

However, research reveals that 65% of insurance executives report progress on AI assistants, but only 29% of customers are comfortable with GenAI virtual agents providing service.

What customers actually want:

Personalized pricing and products—not just faster chatbots. They want insurance that adapts to their lives, not generic policies with automated support wrapped around them.

Pro Tip:

Track "deflection rate" alongside NPS. If your GenAI chatbot resolves 65%+ of Tier 1 queries without human handoff, you've hit the ROI inflection point for customer service automation.

Marketing and Distribution Optimization

Marketing in insurance has traditionally been generic and compliance-heavy. Gen AI enables personalization at scale while automatically checking regulatory requirements.

Key Applications:

- Personalized content creation for different customer segments

- Compliance-checked marketing materials generation

- Advanced customer segmentation using behavioral and sentiment data

- Real-time campaign performance analysis

- Lead scoring and qualification to prioritize high-value prospects

- Agent and broker support tools for faster proposal generation

Insurers can now send targeted home insurance offers right after someone purchases a property, with messaging tailored to their specific situation.

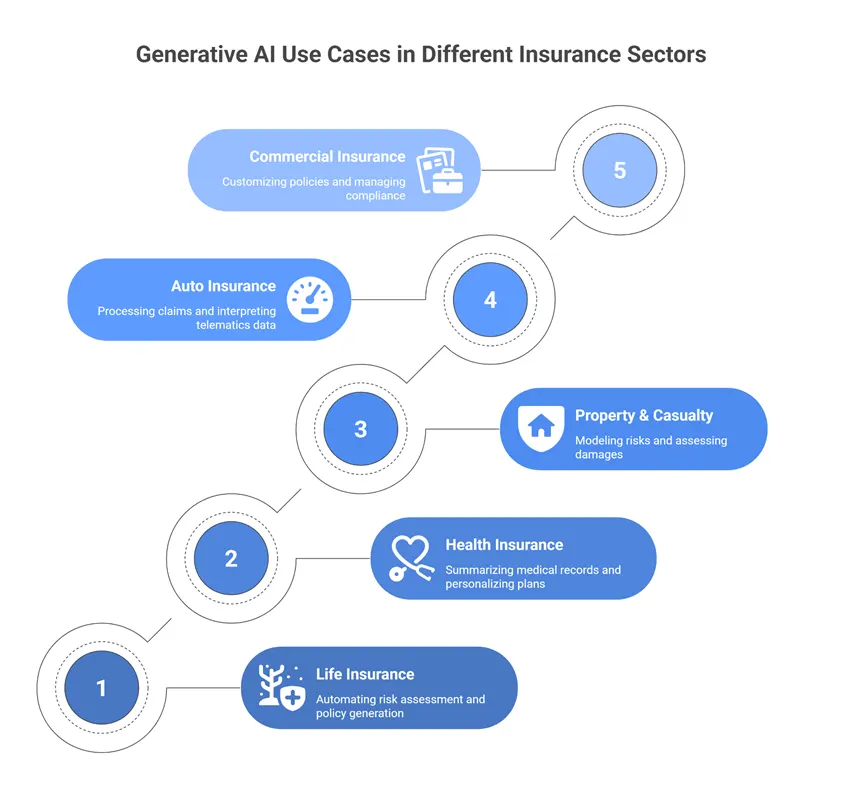

Generative AI Use Cases in Insurance Across 5 Key Sectors

Generative AI in the insurance industry is a stack of models that summarize dense records, generate compliant documents, and simulate risk so teams move faster without adding error or bias creep.

If you run life, health, P&C, auto, or commercial lines, the playbook looks similar:

- Use foundation models fine‑tuned on domain data

- Wrap them with controls (PHI/PII handling, role‑based access)

- Add retrieval for source‑of‑truth grounding, and instrument everything for auditability.

Below are practical, high‑impact use cases in insurance that teams (in any sector) can pilot without boiling the ocean:

| Insurance Sector | Top 3 GenAI Use Cases | Unique Differentiator |

|---|---|---|

| Life | Risk assessment, policy generation, beneficiary comms | Mortality prediction models |

| Health | The top uses of generative AI in health insurance include prior auth, claims adjudication, and plan recommendations | HIPAA-compliant PHI processing |

| P&C | Catastrophe modeling, damage assessment, and inspection reports | Scenario simulation for natural disasters |

| Auto | Photo-based claims, telematics pricing, fraud detection | Usage-based insurance optimization |

| Commercial | Cyber risk assessment, broker submission review, compliance docs | Multi-peril exposure modeling |

To see how insurance leaders are thinking about these applications in practice, Red Hat's industry experts discuss current use cases, governance challenges, and what's next for AI in insurance.

Check out the full video here:

Challenges & Practical Solutions for Generative AI in the Insurance Industry

You’ve seen the splashy demos: chatbots that quote a homeowner’s policy in ten seconds, underwriters who finish a risk memo before coffee gets cold.

The upside is real, but so are the headaches.

Let’s transition now into the real world difficulties and risks of AI, and understand how to solve them.

Technical Barriers

If you’ve ever tried plugging a modern AI tool into an aging insurance core system, you know the pain.

For example, 45.5% of insurers identify integration challenges with new technologies as a major hurdle in modernizing their core platforms.

Also, legacy systems throw up roadblocks such as outdated data formats, siloed systems, batch processing only, and little real-time capability.

— Senior Cloud Architect, Aegis Softtech

Solutions:

- Use API-based integration layers or middleware that sit on top of the legacy stack so you don’t need a “rip-out everything” big bang.

- Adopt a phased modernization strategy. Upgrade critical modules step by step rather than pursuing an overnight core replacement.

- And back this with a decision framework for hybrid architecture: when to modernize the core versus when to work around it.

Here’s a table explaining when to modernize core systems vs. work around them:

| Scenario | Modernize Core | Work Around (Middleware/API Layer) |

|---|---|---|

| System Age | 15+ years, unsupported tech stack | 5-15 years, vendor still provides updates |

| Data Quality | Core data is corrupted, inconsistent formats across modules | Data is clean but locked in proprietary formats |

| Business Impact | Core system failures cause customer-facing outages | Workarounds don't affect customer experience |

| Integration Needs | Need real-time bidirectional sync across 5+ systems | One-way batch data flow or occasional API calls |

| Regulatory Risk | Can't meet compliance requirements (audit trails, data retention) | Compliance is achievable with abstraction layer |

| Budget & Timeline | 18-36 months available, $5M+ budget approved | Need results in 3-6 months, limited budget (<$1M) |

| Tech Debt | Customizations make upgrades impossible | Standard configurations, upgrades still feasible |

| GenAI Use Case | Need to train models on historical data spanning decades | GenAI only needs recent transactional data |

Decision Rule:

If 5+ factors point to "Modernize Core," start phased replacement. If 5+ points go to "Work Around," use API/middleware and revisit in 12-18 months.

Data Privacy and Regulatory Compliance

You’re in the insurance business, and that means heavy regulation. Rules such as the General Data Protection Regulation (GDPR), the Health Insurance Portability and Accountability Act (HIPAA), etc, require that any generative model deployed in insurance be transparent, auditable, and safe.

Generative AI must be able to identify and strip PII, maintain model explainability (so regulators can ask “why this policy/premium decision?”), and support audit trails.

— VP of Data Engineering & Compliance, Aegis Softtech

Solutions:

- Embed fail-safes, ethical thinking, real-time monitoring, and audit logs in your model deployment pipeline.

- Start your rollout with low-risk use cases. Examples include customer FAQs, internal document summarization) before handling high-risk decisions (e.g., life insurance underwriting, health risk scoring).

Organizational Change and Workforce Transition

When you start investing in generative AI, many of your people will feel unsettled. According to a US survey, about 75% of employees believe AI might make certain jobs obsolete, and roughly 65% say they’re anxious about AI replacing their role.

Solutions:

- Invest in reskilling programmes by creating roles such as prompt engineers, AI ethics specialists, and data-governance stewards.

- Recognize that adoption requires twice the effort of building the tech, as firms discover that training, change management, and culture shift matter just as much.

- Training programmes can deliver 20%+ productivity gains per user, especially when they feel confident and empowered.

- Build cross-functional teams that pair business owners and technologists—business-led, tech-enabled.

Cost and ROI Concerns

"Great, we’ll build Gen AI.”

Yes, but at what cost?

Implementation costs, cloud/compute expenses, data prep, integration, and governance layers all add up.

You’ll want a clear view of cost vs. performance and guard against vendor lock-in.

Solutions:

- Adopt modular architecture so you’re not locked into one vendor or siloed stack.

- Begin with minimum viable use cases, prove ROI, then scale.

- Follow a Build–Buy–Wait framework. Buy off-the-shelf solutions for generic tasks (e.g., document summarisation). Build in-house for the core differentiators (e.g., custom risk-scoring model). Wait when ROI is unclear or solutions are rapidly improving.

Quick Decision Guide:

- BUILD → Core business differentiator + unique data/processes

- BUY → Standard function + need speed + proven ROI

- WAIT → Immature market + high cost + uncertain value + rapid vendor innovation

By addressing these four domains—technology, data & compliance, people, and cost/ROI—insurers can turn the promise of generative AI into sustained value.

It’s not enough to “deploy a model”. You must integrate, govern, train, and scale.

The payoff is smarter risk models, faster servicing, and a competitive edge that actually lasts.

6 Traits of Successful Gen AI Insurance Organizations

Leading insurers share common patterns in how they deploy generative AI in the insurance industry. Here's what separates pilot purgatory from production impact:

| Trait | What Winners Do Quick Win | |

|---|---|---|

| 1. Strategic Focus | Pick ONE end-to-end transformation domain (claims, underwriting, or distribution) vs. scattered pilots | Start with the highest claims volume process |

| 2. Build vs. Buy | Build for competitive edge (proprietary data, unique guidelines); Buy for commoditized tasks (CRM, chatbots) | Use the decision matrix above |

| 3. Reusable Components | Create modular "archetypes" (document ingestion engine, intent classifier) that speed future builds | Template your first 3 use cases |

| 4. Hybrid AI Stack | Layer GenAI with traditional AI (predictive models) + RPA for compound value | Connect severity engine → GenAI summary generator |

| 5. Risk-First Design | Involve compliance, legal, and risk teams from day one—not after deployment | Embed kill-switches + audit logs from pilot phase |

| 6. Measure Ruthlessly | Set accuracy, efficiency, and compliance KPIs before launch; monitor continuously | Track 3 metrics weekly: accuracy, cycle time, cost-per-transaction |

Also Read: Generative AI in Manufacturing

How Can Insurers Deploy Generative AI? Roadmap + Free Checklists & Template

Transitioning from AI curiosity to enterprise-scale impact is about precision. The smartest insurers move in phases, each designed to test, prove, and then expand value safely.

Let’s walk through a roadmap that actually works in the real world:

Phase 1: Assessment and Strategy (Months 1-2)

Before a single prompt hits the model, you need to know what you’re working with. Start by running a current-state assessment of your data readiness, tech infrastructure, and team capabilities.

Are your datasets structured? Do your APIs talk to each other? Does your staff understand prompt logic and bias control?

Then, identify high-value, low-risk use cases such as policy summarization, claims triage, or customer query automation. These prove value without regulatory headaches.

Next comes your business case: map ROI projections for efficiency gains and reduced cycle times.

And don’t forget the human side. Establish stakeholder alignment and governance to ensure IT, compliance, and business leaders all row in the same direction.

We have built a practical Readiness Assessment Scorecard to benchmark where your organization stands across data maturity, compliance readiness, and talent. Prioritize where to begin, and where not to.

Phase 2: Pilot and Proof of Concept (Months 3-5)

Now, pick one or two targeted use cases.

Build a minimum viable product (MVP) small enough to manage but real enough to measure.

Define success metrics and KPIs upfront.

We've got a practical insurance-specific KPI dashboard that is simple, actionable, and easy to plug into a BI tool (like Power BI, Tableau, or Looker). It’s designed to track the right metrics for GenAI performance in insurance.

And, run the pilot with a limited user group, gather insights, and iterate.

The key is to avoid pilot purgatory. Set clear graduation criteria that determine when a pilot “earns” the right to scale.

— GenAI Lead, Aegis Softtech

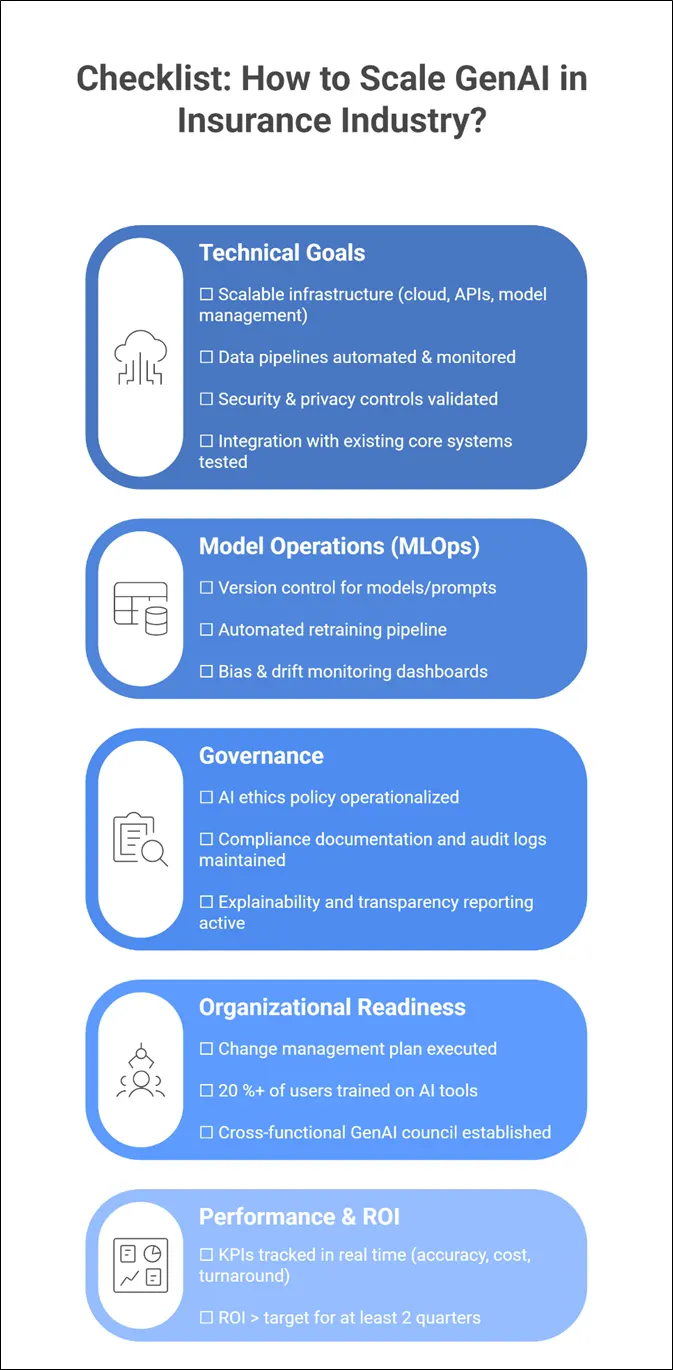

Phase 3: Scale and Optimize (Months 6-12)

Once your pilots deliver measurable impact, it’s go time.

Scale successful pilots into production and develop reusable components (like data connectors, prompt templates, and governance models) to accelerate the next rollout.

Invest in training and change management so your teams evolve with the tech. Create feedback loops for continuous monitoring, fine-tuning, and risk control.

Pro Tip:

Build a "context library" of pre-approved prompts, guardrails, and sample outputs for each business function. This cuts onboarding time and ensures consistent, compliant AI usage.

As you gain traction, expand GenAI into adjacent domains such as underwriting support, fraud detection, and personalized recommendations.

Here’s a checklist that can guide you as to when you can expand from pilot to enterprise deployment of generative AI in insurance:

Goal:

All boxes should be checked before expanding GenAI to new domains or geographies.

Also Read: Generative AI in Software Development

Turn Potential into Performance with Aegis Softtech's Generative AI Services

Generative AI is reshaping insurance fast. But the winners aren’t chasing quick wins; they’re focusing on end-to-end transformation.

Success starts small—assess, pilot, scale—and grows through smart governance, hybrid architecture, and continuous learning.

If you’re ready to move from potential to performance with generative AI in insurance, Aegis Softtech can help you get there. We are smarter, faster, and precise.

With 20+ years of engineering experience, our Gen AI experts design clean, compliant, domain-aligned GenAI solutions, from copilots that speed underwriting to agents that boost service.

In short, we make AI work for your business, not around it.

Frequently Asked Questions

The three D’s of insurance claims are: Delay, Deny, and Defend. The three D’s describe traditional insurer tactics in claim handling. Generative AI in the insurance industry helps reverse this by streamlining processes and improving claim transparency.

The generative AI in insurance market has several emerging trends:

- AI will evolve from automation to adaptive intelligence — real-time underwriting and predictive claims.

- Multimodal AI (text, image, voice) will enhance customer experience.

- Synthetic data and trustworthy AI frameworks will drive safe innovation.

- By 2030, insurers will run on AI-driven ecosystems.

No. Generative AI in insurance will augment, and not replace, claims adjusters by automating repetitive tasks and providing real-time data insights. It will free humans to focus on complex, judgment-based cases.

Generative AI powers policy document automation, claims summarization, underwriting copilots, fraud detection, and customer chatbots. These applications help insurers deliver faster, smarter, and more personalized services.

Generative AI in health insurance automates prior authorizations, adjudicates claims for complex procedures, and recommends personalized health plans by predicting patient outcomes from historical data. It processes medical records while ensuring HIPAA compliance for secure, faster decision-making.